The young have always been considered a relatively unappealing market segment for the banking sector, owing to their limited income. However, when the burgeoning young population steps into adulthood in a few years and becomes wealthier, it will become the prime focus of the banking industry. Unfortunately, it may be too late for traditional banks to gain their business at that point in time because other kinds of businesses (like neobanks) are tapping their future client base young!

Parents Push for Financial Literacy in Teens But Lack Resources

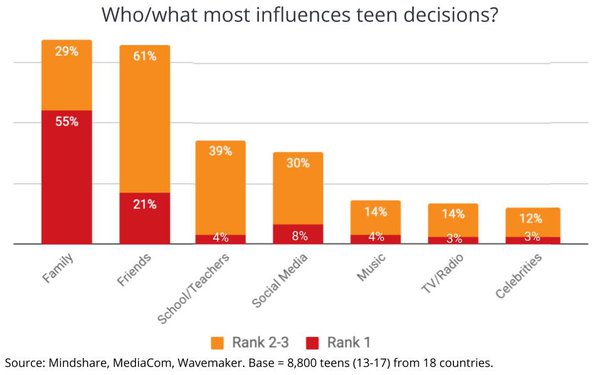

Contrary to the popular belief that today's youth is largely influenced by celebrities and social media, a Group M research found that family and friends continue to remain the driving factor behind their decisions. The findings are based on interview responses from 8,000 teens under parental supervision in 18 countries.

(Source)

(Source)

*But what does this mean for banks? *

A window of opportunity and a battle they are currently losing to various fintech companies that are meeting the demands of millennial parents when it comes to teaching their kids financial literacy. Millennial parents don't want to micromanage their kids' finances. Instead, they want to impart financial lessons at an early age to help their kids develop financial acumen and responsibility before they are old enough to rake up piles of credit card debt. But the traditional banking system doesn't cater to this demand. Here are some of the issues that traditional banks have failed to solve:

- Owing to the lack of junior banking products, parents continue to pay their children pocket money in cash, which gives them little visibility into how this money is spent.

- Children typically depend on their parents' debit cards for digital transactions, which poses security risks. It is also a lost opportunity for parents to give their kids valuable lessons in budgeting and monitoring their digital spending.

- MCC (Merchant Category Codes) controls are not available on all cards, which means parents cannot control overspending on gaming, in-app purchases, or even eating out.

- For children who have bank accounts, the lack of mobile apps for banking or poor digital experiences put off kids from using these accounts.

Junior Banking - Fintechs Rush to Bridge the Gap

While the traditional banking sector continues to wait for teens to grow and bank with them as adults, neobanks have identified the opportunity and are rushing in to fill the gap. Take the example of Muvin, a neobank that offers money management tools and bite-sized content to the youth on their mobile phones to help them learn concepts like savings, expenses and budgeting. The mobile app allows parents to set up an easy-access digital account for kids where they can receive their pocket money and track expenses. Muvin also offers a prepaid cashless card to teach kids how to handle plastic money without falling into a pile of debt. Muvin is just one of the many fintech companies enabling a youth-focused banking experience to help teenagers and young adults gain financial literacy and independence. It’s only a matter of time before these companies will introduce other services like lending and insurance (we all know the WeChat story, don’t we?), scooping away customers from traditional banks. By focussing on the youth, these companies also build strong relations with parents and stand to win their business as well.

So what does this mean for the traditional banking sector that hasn’t seen much evolution since the advent of internet banking?

In modern parlance, a strong call to expand their focus towards the unbanked youth population and upgrade their digital experiences to provide Google’s intuitiveness, Uber’s ease, and Amazon-like customer service. And that's where they lack!

4 Action Points for Building Junior Banking for the Younger Generation

1. Financial Literacy

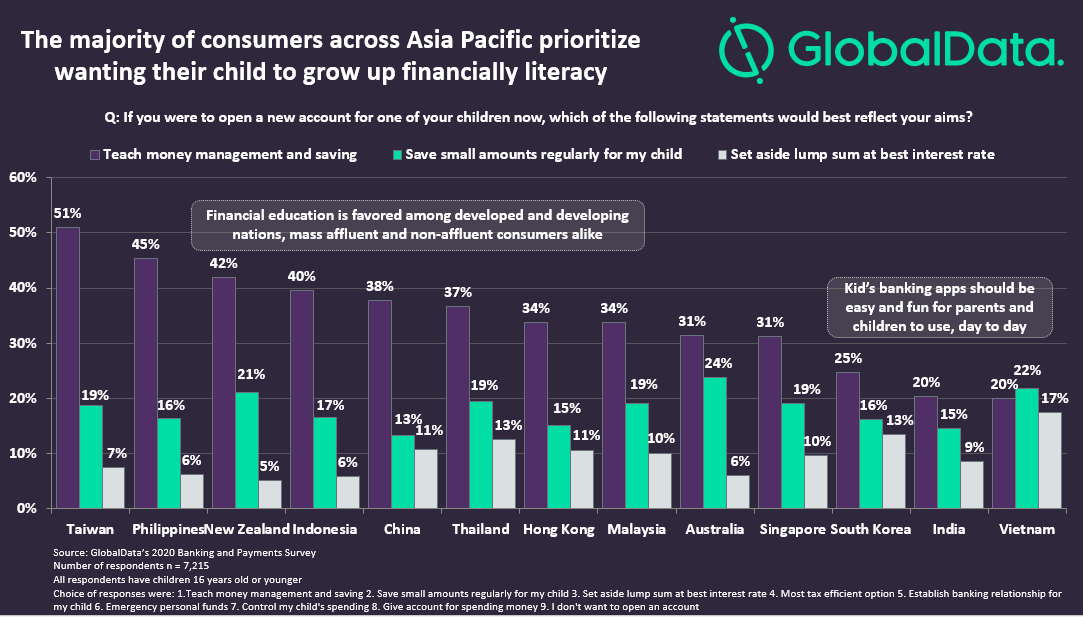

It is a daunting task for parents to make their kids financially literate. The subject is not even taught in schools. But banks can fill this gap, as parents consider them well-suited to offer financial content, according to GlobalData’s 2020 Banking and Payment survey. The survey also showed that “teaching the importance of money management and saving” is the top priority of parents across the Asia Pacific when opening a child’s bank account.

(Source)

(Source)

These results show that educational content should be the prime focus for banks when venturing into children’s banking. Parents will always choose financial literacy over finding a good interest rate. Learning by doing the basic principle, that banks can integrate into their digital experiences to promote financial education, animated videos, stories, quizzes, and real-world experiences make for engaging content that can be gamified with badges and leader boards to promote learning. By offering easy-to-use, educational products for children, banks can establish themselves as "fountains of knowledge" and forge deeper connections with both parents and children, seamlessly expanding their customer base.

__2. Improved Personalisation __

Today’s youth are becoming financially independent a lot earlier as compared to previous generations. However, they don’t want the same banking experience as the generations before them. Instead, they are looking at a much higher level of personalisation and definitely a lot more convenience. Think borderless banking, frictionless customer service and transparent pricing structures. They also want more value – perhaps a breakdown of their spending patterns, suggestions on how to boost their savings, gamified content, loyalty rewards, etc. Offering junior banking services also creates an opportunity to upsell other products. In India, HDFC Bank offers specialised products and services that support younger customers. They have on offer a children’s account to encourage financial literacy in kids and products to support them as they grow older, like education loans and targeted saving plans.

3. Greater Control for Parents

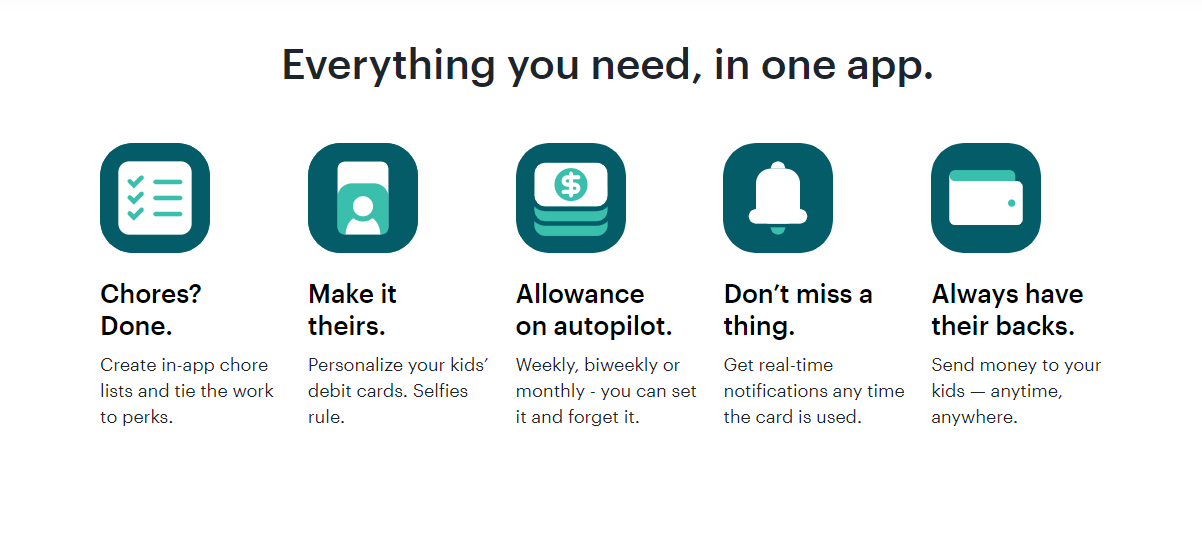

Parents can deposit pocket money digitally into their kids' accounts, track their spending and have meaningful conversations around improving their spending decisions. For instance, the Greenlight debit card and money app provides parents with control over where their kids can spend money. Instead of teaching kids about money the traditional way, parents can use this app to transfer chore money and pocket money directly into their kids’ prepaid debit cards, set spending limits, and teach them how to make prudent financial decisions.

(Source)

(Source)

4. Social Communication

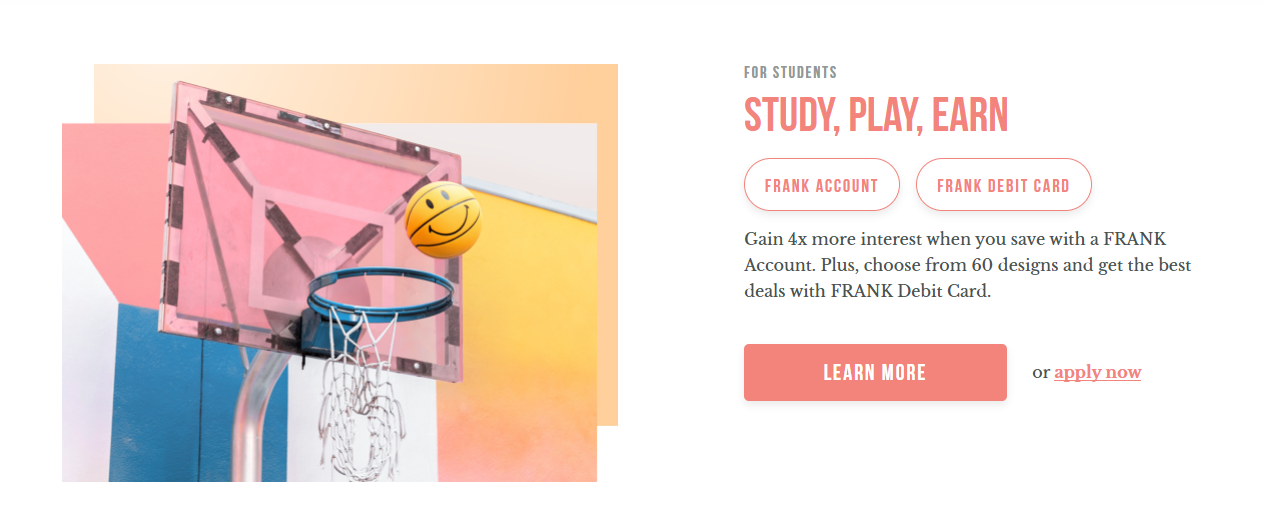

The millennial generation doesn’t necessarily view a bank as a place to keep their money safe. They judge banks on more than just their offerings. Similar to retail, Gen Z is attracted to brands that are cool, fun and socially conscious. It’s true that traditional banks cannot fit into this mould, but they can introduce a sub-brand to attract the youth. FRANK, launched by OCBC in Singapore, is a sub-brand targeting this segment. The branding employs minimal jargon and shows fashionable young people enjoying themselves at work and at home. The name FRANK itself is an adjective for a simple and honest expression that ‘vibes’ with the youth it wishes to attract.

(Source)

(Source)

Earning positive equity by genuinely helping people can also appeal to the youth that takes pride in working with socially conscious organisations. KoinWorks, a fintech company, launched the KoinWorks Cares program to educate users about safe investment options during the pandemic. The company also ran a massive donation campaign and provided a sizeable insurance cover for free to all the donors. The collected funds were used to purchase testing kits for Indonesian people. The campaign was a massive hit in the country that has a significant population under 30 years of age.

The Bottom-Line

Today’s youth is tomorrow’s revenue. Even though this segment has limited income today, they will form a lucrative client base for banks in the near future. Yet, many banks have not yet turned their attention to this age group or taken any firm action to attract them. And, if they don’t, there’s burgeoning competition from companies in the fintech sector who will scoop away this clientele and a major source of future revenue.